Application

PROCEDURE FOR CREATING AND USING CARDS OF INDICATORS FOR ASSESSING LABOR RESULTS FOR A CERTAIN PERIOD

Glossary of basic terms

Auxiliary units- divisions of the enterprise, the result of which is the service maintenance of the main divisions of the plant.

Award group- a group of positions for which the same bonus conditions are established.

Group indicators- indicators for evaluating the effectiveness and efficiency of the work of employees of one structural unit or the enterprise as a whole, aimed at measuring the degree of achievement of the general goals set for this group. A group indicator (usually quantitative) is common to all employees in a given group. The share of group indicators in the overall assessment is determined separately for each group of positions.

Performance evaluation range- values of a quantitative indicator (from minimum to maximum), within which the amount of the premium is determined.

Individual indicators- indicators for evaluating the effectiveness and efficiency of an individual employee, used to measure the degree of achievement of the goals set for him. Individual indicators can be both quantitative and qualitative.

Map of indicators for evaluating the results of work for the position (Further- indicator map) - a set of indicators corresponding to the key areas of responsibility of this position, indicating the weight, range of performance assessment, calculation methodology, objects of assessment, data sources for calculation.

Qualitative (expert) indicators- indicators designed to evaluate the performance of an employee in his position, performed on the basis of expert findings of several persons (experts). Qualitative indicators are calculated in accordance with the methodology for performing an expert assessment of labor results.

quantitative data- data on the company's activities for the assessment period, expressed in specific units of measurement. Used to calculate quantitative indicators.

Quantitative indicators- indicators reflecting the degree of achievement of the target result; expressed in physical or monetary units, as well as in relative form. The calculation methodology and data sources for quantitative indicators are indicated in the individual scorecard for each position.

Object of assessment- one of the criteria for expert evaluation, a qualitative indicator of labor results. Each object is evaluated separately. In the system for assessing the results of a company's work, usually two to five objects of assessment are used for one expert indicator.

Main divisions- divisions of the enterprise, the result of which is the release of marketable products.

Reporting period- the period for which the evaluation of the results of labor is carried out (month, quarter, year).

Assessed- an employee of the company holding a position included in the performance appraisal system. His performance in this position during the reporting period is subject to evaluation.

Evaluator (expert)- an employee of the company included in the system for evaluating the results of work as an expert. Is an internal and / or external client (consumer of the results of labor) of the assessed employee.

Indicators for evaluating the results of labor- indicators of the effectiveness and efficiency of the activities of an individual employee, departments and the company as a whole. Performance indicators are divided into group and individual, quantitative and qualitative.

Bonus (variable remuneration)- additional remuneration, depending both on the results of the work of a particular employee, and on the achievement of the planned results of the company as a whole.

N-1 level employees- employees directly reporting to the director of the enterprise.

N-2 level employees- employees directly reporting to the directors in the areas.

Employees at N-3 level and below- workers subordinate to lower-level managers and ordinary workers.

The actual value of the indicator- the value of the quantitative indicator for evaluating the results of labor for the reporting period, calculated in accordance with the calculation methodology given in the scorecard.

1. Map of performance evaluation indicators (I)

Agreed:

Head master _____________________

Note:

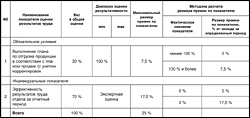

1. For major divisions, it is recommended to use two types of group scores: an enterprise score and a division score. For positions of level N-3 and above, the group indicator of the enterprise is used, and for positions of lower levels, the indicator of the division.

In some cases, instead of a group indicator, the “mandatory conditions” parameter may be used, under which the premium for this indicator is not calculated through algorithms, but is set in a specific numerical expression. An example is the bonus card above.

2. An example of calculating the premium: suppose the performance of the norms was 125.5%

The size of the premium, therefore, amounted to 12.75%.

For auxiliary departments, regardless of the level of the position occupied by the employee, the indicator of the entire enterprise is used as a group indicator (or condition).

3. Individual indicators are determined in accordance with the key areas of responsibility of the assessed employee holding this position. The weight of each individual indicator should be set in the range of 10–60%. In exceptional cases, for piecework workers, it is allowed to set the weight of an individual indicator in the range of 10–90%.

4. The performance evaluation range for each quantitative indicator is determined on the basis of statistical data for previous periods. Such a sample should cover at least four periods. The average value of the sample for the year is taken as the maximum value of the bonus scale.

For a qualitative (expert) indicator, it is necessary to bring the objects of assessment that reveal its essence. The performance appraisal system usually uses two to five appraisal objects for each indicator. Also in the column for this indicator is a list of assessors with an indication of the weight of their opinions in the overall assessment.

Performance scorecard (II)

Click image for a larger view

5. Peer review scores may be increased to five or reduced to zero. Experts fill out an expert assessment questionnaire, then an order is issued to increase (decrease) the score.

With an expert assessment of five points, the maximum percentage of the premium for the indicator increases to 29.2%. Thus, with an expert assessment other than three, the percentage of the premium for the indicator is calculated by the formula:

|

Expert review |

|

For example, department employees are given expert review three points on a five-point scale, then 3: 5 x 29.2% = 17.52%.

6. The bonus card is agreed with the immediate supervisor of the assessed employee or with the head of the structural unit.

2. Rules for calculating the amount of premium by indicator

The methodology for calculating the amount of the premium for each indicator is given on a separate sheet, as an appendix to performance evaluation map and in accordance with it.

To calculate the amount of the premium by a quantitative indicator, such a technique can be used. The performance evaluation range is divided into an even number of intervals (usually from 4 to 10) as follows: first, the middle of the performance evaluation range and the corresponding average bonus for the indicator are determined:

As a result of successive division of the range, we get the n-th number of gaps: , ... .

After the range of performance evaluation is divided into a finite number of equal intervals, the amount of the bonus for the indicator is determined according to the following rule:

x n = b or more

Graphically, this can be represented as follows:

Example. The average percentage of an employee's bonus for certain period is 20%. The weight of the indicator is 30%, the range of performance assessment is 80–120%. In this case, it is advisable to break the performance evaluation range into four intervals: , , , .

The maximum premium for this indicator will be:

For the interval

| 2 | X | 2 x 20% x 30% | = 4,8%. |

For intervals , the calculation of the premium is similar to intervals , .

For actual values of the indicator less than 80%, the premium will be 0%, and for those exceeding 120% - 12%.

Thus, the amount of the premium in this example is determined according to the following scheme:

3. Appendix to the performance evaluation scorecard (I)

Click image for a larger view

Note:

1. To calculate the premium based on a qualitative indicator, it is recommended to use a methodology similar to the method for calculating the premium based on a quantitative indicator.

Graphical representation:

2. The total amount of the premium for the period is calculated as the sum of the actual values of the premium (in percent) for each indicator.

Annex to the performance evaluation scorecard (II)

Click image for a larger view

1. The procedure for calculating the due amount of the premium for the reporting period.

employees of the labor department and wages(OTiZ) the amount of the bonus due for the reporting period is calculated based on the certificates provided by the heads of structural divisions on the fulfillment of group and individual indicators in the prescribed manner.

OTiZ employees bring information about the actual amount of the bonus (including by indicators) to the immediate supervisor of the employee in order to further communicate it to the employees of the enterprise in the prescribed manner.

2. The procedure for revising the maps of indicators for assessing the results of labor for the reporting period.

Reason for making changes to performance evaluation scorecard is:

change in the main functions of the activity of an employee (group of employees), in the event of a reorganization, changes organizational structure, release strength, etc.;

analysis of the degree of achievement of results carried out by HSE employees, identification of indicators for evaluating the results of work that do not have a stimulating effect on the employee (group of employees) in achieving them (them) higher indicators.

4. The procedure for filing mutual claims and the distribution of variable remuneration (bonuses) between labor collectives and employees

Procedure for filing Claims and distribution of variable remuneration (premiums)

1. General Provisions.

This procedure has been developed and introduced in order to:

creation of prerequisites and conditions for highly productive work of labor collectives employed at various stages production process, and in different, but interrelated processes (production, provision, maintenance, management);

development of labor rivalry;

increasing the moral and material interest of labor collectives (teams) and individual workers in achieving high final results.

2.1. The claim is the total expression of wage losses incurred by the team (section, department, service) in the reporting month due to the fault of subcontracting teams that are in industrial relations.

2.2. The claim is drawn up according to the principle of its recognition, i.e. the presence of mutual consent of the labor collectives (the sender and the recipient of the claim) in the form of an Act and is confirmed by the signature of higher managers (sample - Form No. 1).

2.3. The basis for filing a Claim may be: downtime, accidents, poor product quality, interruptions in supply, etc., which significantly affected the results of the work of this team for the reporting month.

2.4. The calculation of the amount of wage losses for the Claims filed is carried out by the OTiZ on the basis of the Act and the data of the relevant departments and services of the enterprise (according to the function belonging), confirming the legitimacy of the Claim.

The amount of wage losses is calculated based on the amount of variable remuneration due to the labor collective - the sender of the Claim in the reporting month in accordance with clause 5.2.2. Regulations on the conditions of remuneration and bonuses for employees.

2.5. Filing a Claim against a labor collective (team) about poor-quality performance of work (services) or non-compliance with the requirements within the framework of production relations between interconnected teams or teams, is expressed in the redistribution of the premium between the sender and recipient Claims in the direction of increase or decrease (respectively) are presented in the following okay.

2.6. To simplify the calculation of the amount of wage losses and the amount of penalties charged for the Claim, the system of labor contribution coefficients (KTV) presented in Form number 2 to this Order, namely:

at the KTV team< 1,0 (penalties) - as a product of the amount of variable remuneration calculated on the basis of individual performance indicators of the labor collective - recipient Claims for the reporting month as a percentage, the amount of salaries of this team and the established KTV, divided by 100%;

when the collective TV is > 1.0- an additional payment is made to the amount of variable remuneration sending team Claims calculated on the basis of individual performance indicators for the reporting month, which is calculated in the amount of penalties received, but not more than 50% of the amount of variable remuneration due team - recipient Claims based on the results of work for the reporting month.

The redistribution of the amount of the bonus between teams, taking into account penalties, is approved by the Director for Personnel and Social Development.

2.7. The Acts of Mutual Claims drawn up in the above manner are submitted to the OTiZ to calculate the amount of penalties in the working order, i.e. as they are presented (do not accumulate at the end of the month).

2.8. Within labor collectives, the amount of variable remuneration is redistributed among employees, taking into account their labor efficiency coefficients (KET), i.e., in proportion to the labor contribution of each employee. KET is established by the direct supervisor of the labor collective (senior foreman, foreman, shift foreman, foreman, etc.) in agreement with the trade union group.

It should be taken into account that:

KET equal to one, is established for employees who did not have any comments from the administration within a month, who completed the production task with high quality, did not violate labor discipline, labor protection rules and other omissions;

KET below one and up to zero is established for employees who worked less productively and intensively than the rest of the team, allowed marriage, violations of technology, labor discipline, labor protection and other omissions;

KET above one up to 1.5, as a rule, is set for employees who have successfully completed all production tasks and tasks of managers; who showed initiative aimed at improving the efficiency of the team; achieved a high quality of work; performing the functions of absent employees; combining professions; successfully performed the most labor-intensive and strenuous work; those who have shown high professional skills, etc.

The heads of the teams receiving the Claim are given the right not to present for bonuses in the reporting month precisely those employees through whose fault the Claim was received (accidents, defects in work, violation technological process, workers and job descriptions etc.).

Form 1

ACT

on making a claim to the labor collective

Click image for a larger view

Form 2

SCROLL

claims and the amount of increase and decrease in labor contribution coefficients

Tab. 1. An indicative list of increasing indicators in determining the KTV for the team - the sender of the Claim

|

No. p / p |

Name Claims |

Value KTV |

| Increasing the intensity of labor, additional costs of working time due to the fault of subcontractors (other structural divisions) |

from 0.1 to 0.3 |

|

| Additional labor costs for the correction of marriage due to the supply of low-quality raw materials, materials, semi-finished products, etc. |

from 0.1 to 0.5 |

|

| Implementation of the most labor-intensive and complex work compared to other structural units (brigades) |

from 0.1 to 0.3 |

|

| Elimination of the consequences of an accident that led to losses in production (failure to meet production standards due to downtime through no fault of the team that sent the Claim) |

from 0.1 to 0.3 |

|

| Development and implementation of new projects aimed at improving production efficiency to make up for losses |

Tab. 2. An indicative list of reducing indicators when determining the CTI for the team - the recipient of the Claim

|

No. p / p |

Name Claims |

Value KTV |

| Excessive downtime of the site equipment due to the fault of subcontractors (service department) for a certain period |

from 0.1 to 0.3 |

|

| Violation of technological discipline, standards requirements |

from 0.1 to 0.5 |

|

| Low quality of transferred finished products (works, services) for further processing (use) |

from 0.1 to 0.3 |

|

| Failure to provide raw materials, materials, tools, electricity and other necessary resources |

from 0.1 to 0.5 |

|

| Non-fulfillment or untimely fulfillment of the requirements for a structural subdivision by related subdivisions |

from 0.1 to 0.5 |

|

| Irregularity of work due to the fault of the structural unit - the recipient of the Claim |

from 0.1 to 0.5 |

|

Form 3

Tab. 1. List of factors affecting the value of the employee's KET

|

No. p / p |

Name Claims |

Value KTV |

| Constant overfulfillment of shift tasks and labor standards | ||

| More high quality jobs compared to other workers | ||

| Reduced equipment downtime against established norms | ||

| Demonstration of initiative by the employee to prevent downtime of equipment and employees | ||

| Combination of professions, expansion of the service area | ||

| Constant performance, along with their duties, of the functions of an absent employee | ||

| High intensity of work, performance of work of increased danger | ||

| Performing the most time-consuming and complex work | ||

| Manifestation professional excellence providing higher labor productivity with high quality of work and reduction of terms of task completion | ||

| Saving basic and auxiliary materials, electricity and other resources | ||

| Development and implementation of new projects aimed at increasing production efficiency |

Tab. 2. List of reducing indicators for determining the KET

|

No. p / p |

Name Claims |

Value KTV |

| Non-fulfillment or poor-quality fulfillment of production tasks | ||

| Insufficient intensity or systematic lag behind the general pace of collective work | ||

| Violation of technological instructions, standard requirements | ||

| Unsatisfactory maintenance of equipment and workplace, violation of equipment operation rules | ||

| Violation of the rules of labor protection and culture of production | ||

| Systematic non-fulfillment or untimely fulfillment of duties in accordance with one's job (work) instructions | ||

| Systematic execution of work with low quality, errors | ||

| Irrational use of raw materials, materials, tools, electricity and other resources | ||

| Increased equipment downtime due to the fault of the employee | ||

| Insufficient production skills, low level of professional skills | ||

| Systematic failure to meet production standards | ||

| Violation of labor discipline, internal rules work schedule, production culture |

In the modern world, HR departments of most companies are increasingly relying on such a method as employee bonuses. With the help of this technique, it is possible to significantly increase the attractiveness of the company for applicants and employees, which in turn makes such a company competitive. Another advantage of employee bonuses is that motivated employees carry out their official duties much more powerful and efficient.

What is employee bonuses

The key method of increasing the material interest of employees in improving performance is the use of bonus payment systems, in which the main part of the salary (payment at the tariff rate, piecework or official salary) is supplemented by financial incentives for the effective performance of their work.

In the general sense premium(from lat. praemium - reward) - financial or other material incentives issued as a reward for success in any activity.

Best Article of the Month

If you do everything yourself, employees will not learn how to work. Subordinates will not immediately cope with the tasks that you delegate, but without delegation, you are doomed to time pressure.

We published in the article a delegation algorithm that will help you get rid of the routine and stop working around the clock. You will learn who can and cannot be entrusted with work, how to give the task correctly so that it is completed, and how to control staff.

In the company, the bonus is a part of the salary, which is focused on motivating employees to improve the quantitative and qualitative criteria of work and leads to a more effective solution of issues in the economic and managerial sphere.

The main objective of bonuses is to improve the efficiency of the company's workflow by stimulating the labor activity of employees.

The organization of bonuses for personnel is based on the bonus systems accepted by the employer in agreement with the trade unions, prescribed in a special Regulation on bonuses and a collective agreement.

All bonus payments can be divided into the following categories:

- According to the final indicators:

- A personal bonus is given to an individual employee for certain achievements.

- The collective bonus is awarded to the department, shop, brigade for their common success.

- Payment form:

- Monetary incentives are issued in financial terms.

- Commodity premium is issued in the form of a valuable gift.

- By accrual method:

- The absolute premium is calculated in a fixed amount.

- When calculating the relative premium, individual interest and allowances are taken into account.

- For the intended purpose:

- A general bonus is paid when high performance is achieved in the course of the company's work process.

- A special type of bonus is awarded for completing special tasks.

- By frequency of transfers:

- Bonuses of a systematic nature are paid systematically.

- One-time bonuses are paid once.

- Award criteria:

- The production bonus is accrued systematically: for a month, a year, at the end of work on a project, etc. These incentives are given to employees as gratitude for conscientious work and performance of official duties.

- The incentive bonus is not related to the job duties of the employee. Such a bonus can be paid for length of service, by a significant date in the life of an employee, after the expiration of the working year.

The introduction of material incentives by the authorities is a contribution to the productive work of the team. As a result of applying the following methods:

- there is competition within the team, the effect of competition;

- the level of self-realization of employees increases, and the feeling of satisfaction from a job well done pushes them to new labor achievements;

- successful in professionally employees do their best to maintain their reputation and by personal example show those who are lagging behind that they have something to strive for.

However, not everything is so prosperous and rosy, there are also disadvantages, for example, creative professions are not the best area for applying monetary motivation. In addition, the conditions for employees of different ages are unequal (some are already near retirement age, while others are young specialists). On this occasion, disputes often arise in the team.

How to develop a provision for employee bonuses

The company must create a bonus system for employees on its own, i.e. the company has the right to accept any kind of incentives for its personnel. Prizes can be both tangible and intangible.

The process of paying bonuses can be fixed in the following regulatory documentation:

- labor agreement(paragraph 5, part 2, article 57 of the Labor Code of the Russian Federation);

- collective agreement (part 2 of article 135 of the Labor Code of the Russian Federation);

- a separate internal document of the company, for example, in the Regulation on bonuses (part 2 of article 135, part 1 of article 8 of the Labor Code of the Russian Federation).

The creation of the Regulations on employee bonuses is a right, not an obligation of the company. Such a Regulation is necessary in situations where the company has decided to further develop the bonus system. If the bonuses are one-time, then for their issuance it is only necessary to issue an order signed by the head in the unified form No. T-11 or No. T-11a, if the bonuses are paid immediately to a group of workers (part 1 of article 8 of the Labor Code of the Russian Federation).

The system of the Regulations on bonuses to employees may consist of the following sections:

- General provisions.

Usually, this paragraph specifies the goals of introducing a provision on bonuses. It is explained at the expense of what financial resources the bonuses are issued and to which funds they relate, to which groups of employees they apply. The list usually includes all staff members and sometimes collaborators. Contractors under a civil law contract are not members of labor relations with the employer, in connection with which they are not included in the list of bonus employees. It is especially necessary to monitor those employees who have not fully worked out the period for which financial incentives are accrued. If all of the above points are not fixed in the Regulations on bonuses to employees, then disputes cannot be avoided.

- Types of bonuses and allowances, as well as indicators of employee bonuses.

In this paragraph, it should be written for what exactly the award is issued, and indicate the indicators of its issuance. The most popular are the following criteria:

- increase in labor productivity;

- improvement of production indicators;

- fulfillment or overfulfillment of the plan established by the company;

- increase in sales;

- performance of other especially important tasks and urgent works;

- implementation rationalization proposals;

- innovation in work, development of new equipment and technologies;

- active participation, significant contribution to the implementation of projects, development and implementation of measures aimed at saving money;

- results at the end of the work.

When determining the type of encouragement, it is necessary to abandon general formulations, for example, “for the result of work”, as they are vague and controversial. An employee can appeal against the size of the bonus assigned to him or its absence, explaining that any result is a result.

- The procedure for calculating the premium and the frequency of payments.

The procedure for calculating a bonus for an employee in order to encourage him depends on various points that must be taken into account. It is also important to know that the calculation process has its own complexities. In this regard, if the director or accountant does not have such experience, it is necessary to contact specialized companies who will provide accounting calculations of this kind.

This section should describe the process for deciding whether to pay a bonus:

- The frequency of accrual and issuance of bonuses (monthly, quarterly, annual, one-time, upon completion of the project).

- The basis for making a decision on the payment of a bonus (a memo from the boss, a report submitted by the employee, a plan for the sale of products and indicators of its implementation, and other documentation on the basis of which the employer will decide on the award of the bonus and its amount).

- Additional steps to agree on the issues of issuing a bonus, which should be fixed in the regulation, are to find out who and in what time frame considers this issue.

- The period of consideration of documents-grounds and the timing of the decision.

- The process of familiarizing with the decision of employees.

- The process of bringing the decision made by the authorities to the employees of the accounting department. Ideally, the transfer of such documentation should be recorded in a separate log.

- Award dates. Typically, an employee receives a bonus on the day of receipt of the salary, established by the employment agreement or local company documentation.

- List of payments for which bonuses and allowances are not made.

Before signing the Bonus Regulations, you should find out which types of payments will not be taken into account when calculating the bonus. This moment is especially popular with employers in the Far North and territories equated to it. For example, the employer decided to accrue bonuses to employees in the amount of 60% of the basic salary. In this situation, it is necessary to fix in the Regulations on bonuses that bonuses are accrued as a percentage, based on the amount official salary employee.

If it is written that the bonus is equal to 30% of the employee’s salary, then its amount will seriously increase, since the salary includes both the official salary and additional payments for irregular working hours, and district coefficient, and a percentage premium. In this situation, deciding to accrue to the employee a bonus in the amount of 6,000 rubles. taking into account the tariff rate of 20,000 rubles, as a result, you can get an amount of 10,000 rubles. And if the company has 200 such employees, then unplanned costs in the organization will amount to approximately 800,000 rubles.

- Final provisions.

This paragraph regulates the procedure for the entry into force of the Regulations on bonuses to employees and the period of its validity. As a rule, the bonus provision is valid until it is canceled or until a new local bonus act is developed and adopted. If it is an annex to the collective agreement or one of its clauses, then its effect ends at the end of the agreement or the provision is extended along with the collective agreement. Pay special attention to the following point: if the bonus application is a section of the collective agreement, then the rules for adjusting the collective agreement are attached to it.

This list cannot be called complete; in each organization, it can be supplemented with items related to the specifics of its workflow. For example, these can be items indicating the categories of employees to whom bonuses and incentives are not paid, sections on material assistance to employees, on additional financial incentives related, for example, to temporary disability, etc.

After the Regulation is developed, it is necessary to coordinate it with the trade union, if any, and approve it from the director of the company in accordance with part 4 of Art. 135 of the Labor Code of the Russian Federation. It is necessary to familiarize each employee with the Regulation under his personal signature (part 3 of article 68 of the Labor Code of the Russian Federation). To do this, it is necessary to attach a piece of paper to the Regulations, in which employees, after familiarization, will sign.

If the employee can prove that all the criteria and conditions for bonuses are met by him, then the company and its superiors of the State Inspectorate of the Russian Federation or the court may be held administratively liable under Art. 5.27 of the Code of the Russian Federation on administrative offenses(Article 23.12 and part 2 of article 23.1 of the Code of Administrative Offenses of the Russian Federation). The amount of penalties is:

- for the director - from 1,000 rubles. up to 5,000 rubles;

- for individual entrepreneurs - from 1,000 rubles. up to 5,000 rubles;

- for a company - from 30,000 rubles. up to 50,000 rubles

Repeated violation will result in:

- for the director official) - penalties in the amount of 10,000 rubles. up to 20,000 rubles or disqualification for a period of one to three years;

- for individual entrepreneurs - penalties in the amount of 10,000 rubles. up to 20,000 rubles;

- for the company - penalties in the amount of 50,000 rubles. up to 70,000 rubles

These measures of responsibility are provided for in Part 1 and Part 4 of Art. 5.27 of the Code of Administrative Offenses of the Russian Federation.

Employee bonus criteria, or how to choose whom to encourage

Bonuses for employees can be carried out both individually and according to a group of established criteria. Specialists identify four main groups of bonus indicators that stimulate workers for individual labor results:

- Quantitative indicators: fulfillment or overfulfillment of production indicators for the production of products and nomenclature, the percentage of fulfillment of production standards, organization of uninterrupted and rhythmic operation of technical equipment, compliance with or reduction of the deadlines for the implementation of repair work established according to the plan, performance of work by a smaller number of employees compared to the accepted standard, lowering the labor intensity of products etc.

- Qualitative indicators: improving the quality of manufactured products, the percentage of delivery of goods from the first presentation, reducing the number of defective products, increasing the grade factor of the goods, etc.

- Saving resources used: budget spending of semi-finished products, materials and resources, fuel, reducing service costs production equipment etc.;

- Rational use technology: fulfillment of the terms established according to the plan for the development of new technical equipment, the implementation of technological discipline, increasing the load factor of technical equipment, etc.

The main disadvantage of the employee bonus system is the possibility of an anti-incentive as a result of illiterate personnel motivation. An indicator chosen in a stimulating role, in reality, can go into the category of anti-stimulus. Example: if the bonuses for employees of medical institutions are set depending on the number of patients who applied to them - the most popular indicator of the work of such institutions - then hospital employees may have a desire to increase the number of patients.

In order to avoid the appearance of an anti-incentive, various methods are used, for example, other indicators are included in the bonus system for employees that can correct the work of the main indicator.

In a scorecard, usually provides for a hierarchy of incentives. Usually this happens either in a simplified version by using 2-3 indicators, or by fixing the mandatory and additional conditions for bonuses to employees, or by establishing the main, basic and additional bonus criteria.

In the first situation, 2-3 performance indicators are formed as incentives for the work process.

In the second situation, the establishment of a systematization of incentives involves the use of bonus conditions for employees. Bonus conditions- quantitative and qualitative indicators of the work process, the implementation of which will provide the employee with financial incentives. If the mandatory conditions are met, the employee will be paid most of the incentive - 60-70%. Fulfillment of additional conditions increases the amount of the promotion. If the mandatory conditions are not met, the reward amount can be reduced to 50%.

The most complicated bonus procedure is provided for when applying the third variant of the hierarchy of incentives, that is, when dividing the criteria into main, main and additional.

The main criterion called the criterion that is considered the most important incentive in the work process of the company and on the observance of which depends almost half or even more of the bonus.

Main criteria 2-3 less significant criteria are named, but also important indicators in the company's workflow. For example, the state of working capital, an increase in workflow productivity, budgetary use of resources, etc. If they are observed, the base bonus increases by 20-40%.

Additional criteria called those criteria that are characteristic of individual professions, private. For example, for an economic position, this may be a rationale for planned calculations, for a seller, compliance with sanitary standards, etc. If they are observed, the base bonus increases by 10%.

The criteria for rewarding employees should be clear, simple and easy to remember for them. There is an opinion that with the complication of the reward system, its understanding worsens and efficiency decreases.

For managers, specialists and employees, bonus criteria are directly related to making a profit. Some experts speak about the fact that it is necessary to take into account in the system of incentives for the heads of companies such indicators as the fulfillment of obligations under contracts, an increase in production volumes, and ensuring the production of products of a modern technological level and of appropriate quality.

The condition of the award as a rule, is the work process during the accounting period and the implementation of the indicators fixed in the plan. Compliance with labor discipline is considered one of the key conditions for bonuses to employees. Employees who have met the planned targets, but committed disciplinary offense, for example, those who were at the workplace in a state of alcohol intoxication or late to work are not eligible for the full financial incentive. Usually they are either completely deprived of the bonus if the disciplinary violation was serious, or they receive less incentive than those employees who have met both the targets and the conditions of the bonus. An employee who has not fulfilled the conditions for bonuses does not receive the right to a bonus or receives the rights to encouragement in the established (basic) amount.

Prize amounts usually set as a percentage of the base salary. Quite popular in the local regulatory documentation on remuneration is the provision for the payment of bonuses in the amount of 40% of the basic salary, although you can also find bonus provisions that involve incentives in the amount of 75% of the basic salary.

The amount of the bonus for a particular employee is established by the employer, taking into account the degree of performance of indicators and bonus conditions.

Expert opinion

Even small bonuses for saving resources are effective

Marina Melchukova,

CEO company "Mediastar", psychologist, Gelendzhik

A couple of years ago, I was the head of the production of furniture on a metal frame. At the workplaces, the employees had a complete mess and dirt, in the reporting documentation - confusion and chaos. Discipline also suffered. In addition, there was a huge overrun of raw materials, resources (electricity) and a significant percentage of defective products. Due to low profitability, the question of liquidating this production was raised. And now I will tell you how we managed to correct the situation.

We started with the implementation of the 5S model. After we cleaned up the production shops, we moved on to the next stage - we established a bonus for savings for employees. Now they had the right to independently decide what materials and spare parts they needed, what they could really save on without losing the quality level, in order to receive financial incentives. Thus, the price of materials for the production of 15 products in the workshop for cutting and processing metal was 1,500 rubles. (cutting disc - 1 piece, peeling disc - one piece, metal pipes - 25-34 and 15 meters).

With the correct use of materials, a worker can save 300 rubles. This can be done at any point: use fewer circles, perform a more competent cutting of the pipe. From the amount saved, the employee received a bonus of 30% (approximately 90 rubles).

In addition to the obvious benefits, there was also no need for a storekeeper who was involved in accounting for materials. And this is a monthly savings of 35,000 rubles. under the article (salary and plus tax deductions from it). Now each production shop independently decided what materials and in what quantity they needed. The brigadiers hung the forms in a conspicuous place, and the employees noted that they had already used up. Based on these indicators, once a month, the foremen made requests for replenishment of materials. Similar forms were kept for manufactured products.

One of the main achievements of this approach is that employees began to realize how the cost of goods is formed. Based on the results of the week, they themselves could calculate how much they managed to save or what was the overrun of materials. All this affected their wages. Employees have become more careful with the materials and technical equipment of the factory. The workshops became clean, discipline developed.

Employees realized that they can influence the level of their wages. Thanks to these measures, the factory was able to reduce the stock of materials in the warehouse and reduce the downtime of technical equipment. Marriage is reduced to the minimum and is possible only in situations where the employee does not comply with the thickness standards or violates the pipe rolling technology.

How to write a memo for employee bonuses

Systematic bonuses, which are provided for by the remuneration system, do not need additional documentation to make a decision on bonuses to employees. The process of assigning and paying such financial bonuses is already provided for by the local regulation on employee bonuses.

In a situation where the manager wants to celebrate the performance of a particular employee by paying an unplanned bonus that is not provided for by the terms of the collective agreement or labor agreement, he can petition the higher management for such a decision. It is for this that the office on bonuses to employees is written. A key component of its content is data on the basis on which the issue of paying a financial bonus for an employee was raised.

The right to make the final decision on employee bonuses - both regular and one-time - remains with the director of the company. Only in the first situation, he approves the results of the distribution of the organization's bonus fund, and in the second, he makes a decision on the accrual or non-payment of bonuses to staff.

Award memo specialist should include the following information:

- the full name of the company in which the employee carries out the workflow;

- Full name of the general director of the company and the immediate supervisor of the rewarded specialist;

- Title of the document;

- general data about the employee, his work experience and a list of his professional successes and achievements;

- a description of a certain situation, as a result of which a decision was made to pay him a bonus (overfulfillment of planned indicators, development and implementation of a rationalization idea, etc.);

- application for an employee bonus;

- date of formation of the memo.

The signature with the decoding of the head of the department certifies the memo. If an employee has multiple bosses different levels, then this document must be signed by each of them.

After application for an award specialist is approved (confirmation is the presence of the director of the company on the form of a memo), the personnel department issues an order, which also needs the signature of the director of the company. After all the documents are drawn up, the accounting officer transfers funds to the bonus employee.

The employee who is responsible for compiling the memo must not forget that this document must contain all the information that allows us to conclude that the employee actually deserves the bonus. A memo can be either printed or handwritten on an A4 sheet.

The most common wording for employee bonuses

The conditions for employee bonuses are determined on the basis of the personnel incentive system that has been formed in the company. When using general bonuses, the key provision is the achievement of specific (in most cases, averaged) indicators, the performance of work within the specified time frame, etc. Upon successful completion of the work plan established in the company, the bonus is issued on the basis of a general order based on the results of a month, six months, a quarter or another term. A list of employees who committed any violations is also clarified. Violations may affect bonus payments.

The wording of orders for the payment of bonuses to personnel in most situations sounds monotonous:

- “for the successful completion of the task (plan, assigned duties)”;

- "for the high quality of the work done";

- “for achieving high results in work”, etc.

If the company applies individually oriented system bonus payments, then such payments may not be related to a time period, but be appointed only for certain individual achievements. In this way, an order to pay a bonus to one employee or a shift, a team, etc. will look like this:

- "for the successful representation of the interests of the company in negotiations with the client and the conclusion of a special profitable contract»;

- "for the performance of a particularly difficult urgent task";

- “for the use of a non-standard (creative) approach to solving the issue”, etc.

For an organization that works for the future, it is important not only to achieve the set targets on time, but also to motivate employees for professional growth, improve the image of the organization, attract more partners to cooperate, strengthen their positions in relation to competitive companies. Such tasks can be solved in different ways, including by taking into account the personal successes of employees, to stimulate which the bonus system is oriented.

Successful participation of employees in various festivals, competitions, developmental events is a plus for the image of your company. There is logic in the organization of competitions within the company with subsequent financial incentives. With a competent approach, the economic result from increasing the professionalism of employees, improving working conditions and greater coherence of the team will be much higher than the money spent on paying bonuses.

Forms for employee bonuses in such a situation, they can simply contain information about the success of employees:

- "for participation in the competition of professional skills";

- "for representing the organization at the All-Russian festival";

- "for winning the football competition among the specialists of a law firm."

Another method that can improve relations in the company's team and increase the level of responsibility for the result of each employee is the payment of individual material incentives dedicated to special dates in the life of an employee (wedding anniversary, birth of a son or daughter, etc.).

A key aspect of the organization's activities is the desire to retain highly qualified and experienced employees. Rewarding employees for loyalty to the organization, many years of effective work in it, bonuses for family dynasties, creating conditions for their emergence - all this has a serious impact on the company's workflow.

How to issue an order for employee bonuses

Employee bonus order can be completed by filling out the following forms:

- unified forms T-11 and T-11a, which are approved by the resolution of the State Statistics Committee Russian Federation dated 05.01.2004 No. 1;

- free-form form, generated and approved in the local documentation of a particular company.

In all these situations, the order will have legal force, since from 10/01/2013 the need to apply strictly unified forms for such an order has been canceled. Both options have their own merits.

The use of Form T-11 means:

- saving the time period spent on the formation of your own form;

- ease of use, which is displayed, for example, in the fact that uniform forms are already hammered into accounting software;

- compliance required details and no risk of claims from state regulatory inspections.

The advantage of using your own form for a company is the fact that it is developed “for itself”, that is, taking into account the specifics of the organization. In your own form, you can enter the necessary details and delete the extra ones.

But in any situation, the form of the order for bonuses to employees must include the data required for this kind of documentation (see paragraph 2 of article 9 of the Federal Law “On Accounting” dated December 06, 2011 No. 402-FZ):

- Title of the document;

- the date of its formation;

- Company name;

- the content of the fact of economic life with the designation of its value and units of measurement (for example, a cash bonus in the amount of 10,000 rubles, etc.). For this situation it says:

- Name of the employee receiving the award;

- the name of his position and the structural unit in which he works;

- motive for the appointment of financial incentives;

- form of encouragement;

- the amount of the premium;

- on whose behalf the promotion is made;

- the title of the position, full name and signature of the official responsible for the performance and / or registration of the transaction / event;

- signature of the director of the company.

Rostrud, in its letter dated February 14, 2013 No. PG / 1487-6-1, additionally confirms the possibility of commercial companies using free forms of primary accounting documents containing the details specified above.

Registration of bonuses for employees using a unified form involves the following stages:

- Submission of a memorandum on bonuses to the director of the company.

- Formation of an order for employee bonuses.

- Familiarization of the employee with this order under the signature.

- OKUD codes (0301026 - code unified form) and OKPO (depending on the form of ownership of the employer);

- Document Number;

- indication of the motive and type of employee incentive;

- an indication of the presentation for the award;

- the mark “the employee is familiar with the order”, certified by the signature of the employee.

In order to write out a bonus to a separate group of employees, the T-11a form has been developed, the content of which is identical.

When drawing up an order on bonuses for employees, you need to know some of the nuances of the bonus process:

- Familiarization of the employee with this document against signature is mandatory, since the bonus is an integral part of the salary, and the director of the company, in accordance with Article 138 of the Labor Code of the Russian Federation, is obliged to inform the employee about the components of his salary.

- Familiarization of several employees with the order at the same time means disclosure by them of information on the amount of financial incentives assigned to each of them. This, in turn, means that before drawing up an order to reward employees in the T-11a form, you need to make sure that all employees have written consent to the transfer of their personal information within the company (this is required by Article 88 of the Labor Code of the Russian Federation and Part 1, Clause 1 Article 6 of the Law "On Personal Data" dated July 27, 2006 No. 152-FZ.)

- The amount of the payment is reduced or raised by the head of the company at his will, except for those situations where the issuance of a fixed bonus is a legal obligation specified in the employment agreement.

Mistakes in the process of drawing up an order for bonuses to employees can be costly for the director of the company, since it is practically impossible to return an overpaid or mistakenly appointed bonus, as the experience of the Supreme Court of the Russian Federation says. The decision of the Presidium of the Armed Forces of the Russian Federation dated September 15, 2010 in case No. 51-B10-1 specifically notes that the salary overpaid to an employee through no fault of his and not in connection with a counting error is not subject to return to the employer.

At the same time, in the ruling dated May 28, 2010 in case No. 18-B10-16, the Supreme Court of the Russian Federation noted three exceptional situations when it becomes possible to recover excessively paid wages and bonuses from an employee:

- If a financial incentive is over-issued due to a counting error.

- If the commission labor disputes recognizes the guilt of the employee in inaction or failure to comply with labor standards.

- If the bonus is excessively issued due to the employee's unlawful actions (this point must be established in court).

The most popular basis for rewarding employees is the achievement of high performance indicators during the work process. But this wording may sound differently, depending on what is indicated in the bonus provision or in the order of the director of the company (if such a moment is not discussed in the bonus regulation).

You should also pay attention to the fact that the law does not regulate the obligation of the employer to acquaint the employee with the bonus order, but the standard forms that were approved by Resolution No. 1 this procedure provide. If there are no signatures of employees in the bonus order, the company may be issued comments from the GIT.

Bonuses and discounts for employees

Employee deduction possible only in a situation where he committed a disciplinary violation. Bonus deduction - this is the deprivation of the full or partial amount of the bonus that is paid to the employee along with wages.

You can partially deprive the bonus, for example, in the following cases:

- disorder in the employee's workplace;

- failure to comply with safety regulations;

- the presence of complaints from customers;

- allowance for inaccuracies in reports;

- not ensuring the safety of goods and materials, etc.

At the legislative level, such punishment as deprivation of the bonus is not provided. There are 3 types of disciplinary punishments. All of them are listed in Art. 192 of the Labor Code of the Russian Federation: warning, reprimand, dismissal. And about deprecation - not a word.

The Labor Code of the Russian Federation provides the employer with the opportunity to provide for such punishments for certain groups of employees in their local documentation, but it is not worth writing directly about bonus deductions. It is better to simply indicate the conditions on the basis of which an employee can receive financial incentives and proceed from the opposite: violated / did not violate any provision.

When signing an employment agreement with an employee, the wording on the components of wages is of great importance.

|

Wording |

Interpretation |

|

Salary includes salary, allowances and bonuses |

Considered payments - part of the pay, not the promotion. Therefore, the employer does not have the right to take them away from the employee, otherwise he will be held accountable. The legal grounds for withholding wages are listed in Art. 137 and 138 of the Labor Code of the Russian Federation. |

|

The contract says that the salary consists of a constant (salary + allowances) and a variable (bonus) parts |

Payments have the status of incentive bonuses. If the conditions of the internal regulations are not observed, the employee is simply not assigned a bonus. To do this, if necessary, provide a link to internal document, with which the employee must familiarize himself under the signature. |

Creation of a reward system for employees - difficult task. Employers often make mistakes that have negative consequences.

Benefits of using a reward system:

- increasing the level of efficiency economic activity company or individual entrepreneur;

- increased responsibility on the part of employers and staff;

- improvement of labor discipline;

- the moment of collective responsibility has a positive effect (because of one person, the whole team can be punished);

- an opportunity for the director of the company to monitor deviations, analyze the situation and make competent decisions based on the data received.

Disadvantages of using the bonus deduction system:

- the psychological climate is deteriorating, the emergence of controversial and conflict situations within the team or a decrease in loyalty on the part of managers;

- in perspective bonus deduction can become a barrier to the full disclosure of the employee's potential;

- this system focused on achieving the overall goals of the company, in connection with which the personal interests of employees may not be noticed.

Cast employee bonus system sample consider the following example.

The Antares company set goals for the production department:

- Volume: 1900 pieces per month.

- Compliance of goods with quality standards.

- Reducing costs without sacrificing quality.

- Timely delivery of goods.

On the basis of these goals, indicators were formulated, in case of deviation from which employees will not be paid a bonus. They included:

- the volume of goods that must be in stock at a certain time;

- percentage of plan completion;

- conformity of the quality of the goods with the established standards;

- compliance with the norms of consumption of raw materials and resources.

An additional condition was also announced: for the return of goods, the head of the shop is subject to deprecation as a percentage of the calculated amount of wages.

How to issue an employee deduction

The company is obliged to competently fulfill all the formalities when accruing or reducing the amount of the bonus. This moment is written in employee deduction order. A single template for this order in our country is not fixed at the legislative level; therefore, it is compiled in an arbitrary format. Required condition - an indication of the reason on which the employee was deprived of additional payment.

You should pay attention to the following point: given order the deduction of bonuses for employees should not be reminded of an act that fixes a disciplinary violation of an employee. Its content should be clear and concise, not ambiguous.

When compiling the text of this order, the phrases “deprivation”, “violation” should not be used. It would be more literate to write "decrease", "non-fulfillment of planned indicators".

The process of de-bonding an employee requires the fulfillment of two conditions:

- the company has a provision on employee bonuses, which fixes all the terms and subtleties (from 01/01/2017, small businesses have the right to carry out the work process without them, if these conditions are spelled out in the labor agreement);

- manager's decision deprecation issue an order (this order must be signed by interested parties).

In a situation where the organization illegally de-bonded employees and this is documented, it will be held administratively liable under Article 5.27 of the Code of Administrative Offenses.

Expert opinion

Reimbursement must be justified

Dmitry Gofman,

owner and head of the company "Techservice"

Under no circumstances should it be brought to the point that someone from the staff has the idea that the reason for not paying the bonus was the need of the CEO to buy himself new car. For example, our company has created a special fund for bonuses to employees - financial resources from fines are transferred there. Every employee of our company knows that this money will be paid to those who actually earned it. Thanks to this method, I got rid of situations in which bonus deductions are perceived as a way to save money on employee salaries.

Typical employee bonus mistakes

Mistake 1.Bonuses are not related or weakly related to the performance of a specialist.

In most companies, bonuses are issued to all employees automatically, as a bonus to the main salary. Or managers set the approximate amount of payments, in no way substantiating this point. The criteria for the effectiveness of the workflow of specialists in this approach are not fixed or are completely independent of the results of the work of the staff.

Error 2.The award acts as an intimidation and punishment for employees.

If one of the company's staff did not perform their duties properly or violated something, then they either receive a partial bonus or do not receive it at all. This method leads to the fact that employees are afraid to break something, are often in a stressful state and lose interest in working effectively. There are two types of incentives for employees:

- material;

- intangible.

Mistake 3.Bonuses are meager and do not motivate staff to work effectively.

The opportunity to receive a bonus motivates staff only when its size is at least 20% of the basic salary. It is necessary to fix a different ratio of the bonus percentage and the basic salary for positions of different levels.

Mistake 4.The specifics of the employee's workplace and the structure of staff motivation are not taken into account.

For employees whose workflow result depends only on their personal work (for example, sales managers, sales representatives etc.), it is logical to fix the percentage of the bonus part and the basic salary in favor of the bonus. And for employees who occupy functional positions (for example, accountants, secretaries, lawyers, etc.), it is logical to fix the ratio in favor of the basic salary.

Mistake 5.A long period of time between achieving results and rewarding employees.

Naturally, the bonus, which is paid every time after the end of the working year, is not an incentive for employees at the beginning of this year.

Mistake 6.There are no accepted targetsKPIs.

In a company in without fail KPI planning criteria must be adopted. It is also necessary to reward employees for above-standard performance indicators. And if such indicators are not accepted, then how and for what is the premium calculated?

Mistake 7.The established targets are either unattainable at all, or are achieved elementarily.

In both situations, employees are not motivated to perform their job duties effectively. If the indicators are prohibitively high, then employees lose hope of ever reaching them. And if it is very easy to achieve them, then the employee reaches the indicators in a fairly short time and loses interest in further actions.

Mistake 8.The reasons for deviations from the indicators are not analyzed and no measures are taken to improve them.

You should systematically carry out a "debriefing" with employees in order to find the reasons that prevent the implementation of the plan. This will not only contribute to giving an objective assessment of the current situation, but will also help to eliminate these causes.

Mistake 9.Financial bonuses are not supported by moral rewards.

Verbal praise without a bonus will also make few people happy. But the effect of the financial bonus will be much brighter if the manager finds the right words, adequately evaluate the work of a specialist and praise him publicly.

Information about experts

Dmitry Gofman, owner and director of Techservice. Dmitry Gofman graduated from the Chelyabinsk Polytechnic Institute (Faculty of Instrument Engineering, Department of Computers). Second higher education received at the Department of Personnel Management of the International Faculty of the Yuzhnouralsk state university. Head of the IT service of the Chelyabinsk branch of the insurance company Energogarant. Head of the IT department of the Chelyabinsk branch of the Non-State Pension Fund of the Electric Power Industry. Head of the S. W. I. F. T. Chelyabinvestbank group. Owner and head of Techservice company. Techservice has been operating in the market of IT outsourcing services in Chelyabinsk since 2001. The company's clients are both enterprises of the city and region, as well as federal companies and government agencies. Number of employees - 15 people. Annual turnover - 10 million rubles.

Marina Melchukova, CEO of MediaStar, psychologist, Gelendzhik. LLC "MediaStar" Field of activity: consulting services in the field of psychology and management Number of employees: 27.

The bonus begins with an assessment, and you also need to remember the basic principle: the variable part of the salary is designed to stimulate labor activity and should encourage the achievement of above-standard results. And you should always remember that the bonus is not part of the salary. After all, the deprivation of the bonus in this case creates stress, conflicts and leads to demotivation of the staff.

The performance related pay (PRP) system is based on a personnel assessment procedure based on key indicators efficiency (KPI). However, in order to introduce such a system into management practice, simple and reliable methods should be developed that establish a relationship between the employee's KPI values and the value of the variable part of the salary.

Personnel assessment by KPI

Previously, our magazine published a methodology for assessing personnel by KPI, based on a combination of current assessment results and competencies of employees. Let us briefly recall its main provisions.

For each position in the organization, on the basis of the employee's service functions, two models (tables) are developed - results and competencies. The first lists all performance criteria for performance evaluation: quantitative and qualitative, individual and team. In the second - the competencies required for this position: corporate (common for all staff of the company), managerial and expert (vocational). From these two models, 5-7 key indicators (of any type) are selected to assess the results and competencies of an employee in the coming month (quarter or other reporting period- depends on the position level) and are recorded in a personal performance table (see Table 1). At the same time, competencies are “equated” with the qualitative results of the employee’s activities. Each of the selected indicators, in accordance with the priorities of the immediate supervisor, is assigned a weight - from 0 to 1 (the total weight should be 1).

Table 1. Personal performance

|

Key indicators (KPI) |

The weightKPI |

Base |

Norm |

Target |

Fact |

Partial result, % |

For all indicators, three “performance levels” are set:

1. Base - the worst admissible value ("zero" point), from which the countdown of the result begins.

2. Norm - a level that must necessarily be achieved taking into account the circumstances (for example, the situation on the market), the characteristics and complexity of the work, and the capabilities of the employee. This is a satisfactory indicator value.

3. Purpose - above-standard level to which it is necessary to aspire.

At the end of the month (quarter), the actual KPI values are evaluated. At the same time, quantitative indicators are measured on a “natural” metric scale, and qualitative indicators are measured on an ordinal 100-point scale. With its help, you can be flexible in assessing quality KPIs by setting “reference points”, for example: base - from 0 to 20, norm - from 40 to 60, goal - from 80 to 100 points. At the same time, assessments must be “deciphered” so that employees understand exactly what results internal customers expect from them.

After evaluating the actual value of KPI, a particular result of work on this indicator is determined in accordance with the formula:

This result reflects the degree of fulfillment or overfulfillment of the norm. So, if the actual indicator is below the norm, then the partial result for it is from 0 to 100%. If the “fact” exceeds the norm, then the partial result is above 100%.

After evaluating each indicator, the employee's rating is determined. To do this, particular results (in percent) are multiplied by the weight of the corresponding KPIs and added together. The result is a "weighted average" performance ratio, reflecting (in percent) the overall performance of the employee for the reporting period, taking into account the importance and actual values of all his KPIs. If the coefficient is more than 100%, this indicates a person’s high performance (above the norm), if less, it means that the norm has not been achieved for some or even all indicators, and the overall result of the work is below the established level.

Next, you should link the received estimates and the amount of the employee's bonus. To do this, it is necessary to remember the basic principle of bonuses: the variable part of the salary is intended to stimulate the labor activity of people and should encourage them to achieve above-standard results. AT Russian practice it is not uncommon for the bonus to be considered in fact as part of the salary and paid "automatically" when the plan is fulfilled. If the employee does not reach the standard indicators, then he loses the bonus in whole or in part. This practice creates nervousness, stress, conflicts and leads to demotivation of the staff. The variable part of the salary should encourage people to achieve higher results compared to the normative ones. And for the implementation of the plan, the employee should receive a salary. It is important that the fixed part of the salary remains constant! Based on these considerations, we will consider two ways to calculate the bonus if the employee's KPI estimates are known.

The first way to calculate the premium

The variable part of the salary (performance bonus) is calculated as a percentage of the official salary using the employee's performance ratio according to the formula:

Of course, this formula is applicable only to those employees whose performance ratio is above 100%, i.e. who have reached above-standard indicators, taking into account the values of all KPIs and their weights. Otherwise, these persons do not receive the bonus. The amount of the payment is limited by the employee's bonus fund.

Consider an example. The work of the shop manager for the past reporting period (month, quarter, half year, year) was evaluated according to five key indicators (see Table 2).

Table 2. Premium calculation example (method 1)

|

Key figures |

Weights |

Base |

Norm |

Target |

Fact |

Result |

|

Volume of production |

3 million rubles |

5 million rubles |

6 million rubles |

5.5 million rubles |

||

|

Share of defective products |

||||||

|

150 thousand rubles |

90 thousand rubles |

60 thousand rubles |

75 thousand rubles |

|||

|

Performance ratio: |

||||||

|

Job salary: Performance Award: |

||||||

Suppose that the official salary of the head of the shop is 40,000 rubles. Then his bonus based on the results of work will be 9.3% of the salary: 40,000 rubles. × 0.093 = 3720 rubles.

As can be seen, for two indicators (“share of production by assortment” and “satisfaction of internal customers”), the results were below the standard. However, the overall result (109.3%) is above the norm, and therefore the employee is given a bonus based on performance.

Thus, the bonus is calculated as a percentage of the official salary, depending on the employee's performance ratio.

The second way to calculate the premium

The total performance bonus is calculated on the basis of the employee's bonus fund as the sum of "private" bonuses earned for each KPI separately. If the size of the bonus fund is known, then the maximum bonuses for all KPIs are first determined depending on their weights:

Then the actual premium for each KPI is calculated as a fraction of the maximum premium, depending on how much the actual value this indicator exceeds the norm:

This formula is applicable only for those indicators for which the "fact" is greater than the "norm". Otherwise, the premium for this indicator is not charged. Then the private bonuses for all KPIs are added up, and the total employee bonus is displayed:

Let's go back to our example. Suppose that the employee's bonus fund is 40% of the official salary, i.e. 40 000 rub. × 0.4 = 16,000 rubles. Then, when using the second method of calculating the bonus, the personal performance table will be different (see Table 3).

Table 3 Premium calculation example (method 2)

|

Key figures |

Weights |

Norm |

Target |

Fact |

Max. premium |

Fact. premium |

|

Volume of production |

5 million rubles |

6 million rubles |

5.5 million rubles |

|||

|

Share of production by assortment |

||||||

|

Share of defective products |

||||||

|

Logistics costs |

90 thousand rubles |

60 thousand rubles |

75 thousand rubles |

|||

|

Satisfaction of internal customers |

||||||

In this case, the maximum bonus for each KPI is determined as a share of the bonus fund in accordance with the weight of this indicator and is accrued upon reaching its target value. For example, for the criterion "output": 16,000 rubles. × 0.35 = 5600 rubles. The same is true for other indicators. In addition, the actual premium for each of them is charged only if the "fact" exceeds the "norm". So, in the above example, for two indicators - "share of production by assortment" and "satisfaction of internal customers" - the standard is not met, so the premium is not accrued. For other indicators, the premium is calculated as follows:

If we add up the actual bonuses for all KPIs, we get the total employee bonus: 2800 rubles. + 800 rub. + 800 rub. = 4400 rubles.

Thus, the premium for each KPI is calculated as a share of the maximum premium, depending on how much the actual value of this indicator exceeds the standard one.

Choice of method

Let's figure out which of the two methods of calculating the premium described above is preferable.

First way - tougher for employees, because it hides a "penalty" for failure to comply with the norm for certain KPIs. If, according to these performance indicators, the result is less than 100%, then the performance coefficient decreases and, as a result, the employee's bonus decreases. Thus, the first way of calculating it stimulates people to a greater extent to pay attention to all indicators, and not just the most important ones. However, it should be borne in mind that the base KPI values should not be overestimated or underestimated. Otherwise, this may lead to the fact that the result (in percent) for these indicators will be inadequately high, if the "fact" turns out to be even slightly more than the "norm", or too low - otherwise. It is clear that this will distort the performance ratio. In other words, the range between "base" and "norm" should be wide enough to increase the robustness of the valuation and premium calculation results.

Second way - softer and "democratic", because it does not imply a "fine". As noted above, the premium for indicators for which the norm is not reached is simply not charged.

On the one hand, this is good, because the threat of punishment to many people is annoying and demotivating. In fact, the "penalty" for not meeting the norm is a hidden deduction from the permanent part of the salary, which contradicts one of the basic principles of wages: the permanent salary must remain constant. If the standard is not met, one should not blame the person, but figure out why this happened. After all, in any organization everything is interconnected, and the reasons can be very diverse. And the award should not be a means of punishment for omissions, but an instrument of encouragement for achievements.

On the other hand, this is bad, because employees may simply ignore some indicators that they “do not like”, or do not make any efforts to fulfill their duties if they realize that they are not coping with the standard. Due to the fact that the "automatic" punishment is not included in the calculation of the bonus, the burden on the immediate supervisor increases. To avoid this, the leader must work with subordinates, find out the reasons for low results and motivate people in other ways, primarily intangible.

Stimulus (lat. stimulus - goad, goad) - an external impulse to action, a push, a motivating reason.

Stimulation of labor involves the creation of conditions (an economic mechanism) under which active labor activity, which gives certain, pre-fixed results, becomes a necessary and sufficient condition for satisfying the significant and socially conditioned needs of the worker, forming his labor motives. Incentive purpose - not in general to encourage a person to work, but to encourage him to do better (more) what is due to labor relations.

motive - this is what causes certain actions of a person, his internal and external driving forces.

AT motive structure labor includes:

the need that the employee wants to satisfy;

a good that can satisfy this need;

labor action , necessary to receive the benefit;

price - costs of a material and moral nature associated with the implementation of a labor action.